Annual audit of finances

Paperwork should back up all transactions insofar as possible. In particular, invoices and receipts should be retained to explain items of expenditure. These should be neatly filed in chronological order to make the auditors’ roles as easy as possible.

The Treasurers Statement should be reconciled with the bank statements, especially the closing balances.

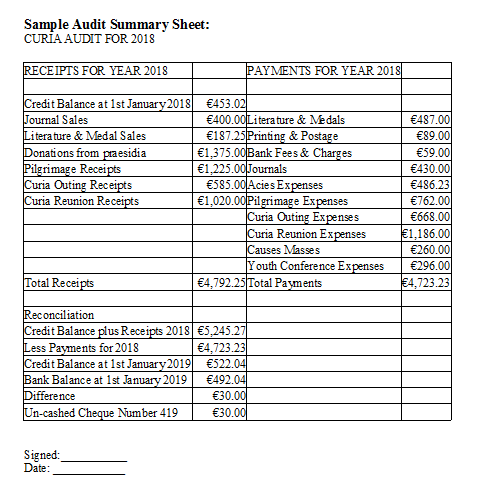

The audit is largely a checking exercise. However a one-page summary of the councils finances for the year is very desirable. This typically gives the opening and closing balances and categorizes the sources of income (donations, contributions from praesidia and lower councils, sales of literature, cover-charge for events etc.) and the outgoings (purchase of literature, cost of hosting events, visitation expenses etc.). See example below.

The one-page summary is something which can and should be presented to the next highest council so that the latter can fulfill its supervisory role.

Higher councils should seek assurances that the audit has been done for the previous years’ finances and request that the summary sheet be forwarded along with the names of the auditors and their position (either as legionaries or as financial professionals).

Paperwork should be retained for whatever period of time is stipulated by local legislation; in the absence of a specified time period, six years is recommended.